Now that you have health insurance, you may be wondering what’s covered and what’s not. By law (namely, the Affordable Care Act — ACA), certain preventive services must be covered at 100%. This means no copayment, no coinsurance charge, and regardless of whether or not you have met your annual deductible. You must receive these services from an in-network provider for your plan to cover 100% of the charge. Preventive

Preventive vs. Diagnostic Medical Services Under the Affordable Care Act

The Affordable Care Act (ACA) mandates that all qualified health insurance plans (except grandfathered plans purchased prior to March 23, 2010 and still in place) include coverage for ten essential health benefits. That does not mean these medical services are necessarily free, merely that your health insurance will cover some or all of the cost. But certain preventive services are free. This means your health insurance must cover 100% of

What is the Employer Mandate?

One of the provisions of the Affordable Care Act (ACA) is the employer mandate. Employer Mandate Companies with 50 or more full-time or full-time equivalent employees must offer full-time employees and their dependents (i.e., children up to age 26) coverage that is affordable* and provides minimum value**. * affordable = employee pays no more than 9.5% of his/her household income ** minimum value = plan pays at least 60% of

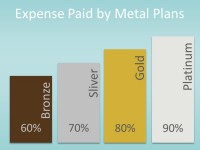

Metal Plans Under the Affordable Care Act

The Affordable Care Act (ACA) created four new designs for health insurance policies. You may have heard policies referred to as “metal plans.” This is because each design is named after a metal: Bronze | Silver | Gold | Platinum The four metal plans are distinguished from one another by their actuarial value. Actuarial value (AV) is the average amount of covered health care expenses that will be paid for

Immigrants and Health Insurance Under Affordable Care Act

Prior to the Affordable Care Act becoming law, many immigrants living in the United States — even those living here legally — did not have good access to affordable health care. But under the new law, immigrants who are in the U.S. legally can now buy health insurance — and qualify based on income for premium subsidies and cost reductions — through their state’s health insurance exchange. (Some states, like

My New Job Offers Health Insurance, but Can I Still Stay on My Parent’s Policy?

Yes*. Just because you are eligible for coverage through your employer does not mean you cannot stay on your parent’s health insurance plan — that is, of course, if you are age 26 or younger. If your parent’s plan seems like a better fit for your family’s budget, lifestyle, or health care needs, staying on your parent’s plan may be the best option for you! *Note, the only exception would

If I Currently Have COBRA Can I Switch to a Marketplace Plan?

COBRA, which is known by most as continuation of benefits, stands for the Consolidated Ominbus Reconciliation Act. Under this 1985 law, covered employees and their dependents who lose health insurance because of one of a series of qualifying events* are entitled to purchase continuation of that coverage. COBRA however, is typically very expensive. Now that the Affordable Care Act (ACA) is here, many people who qualify for COBRA can find

IRS Says Employers Can’t Give Employees Money and Send Them to the Exchange

A recent ruling by the Internal Revenue Service (IRS) addresses a growing trend among employers who, in an effort to avoid the rising cost of providing health insurance, have opted to contribute money towards their employees’ individual health insurance premiums rather than provide group coverage for their workforce. Employees then use that money — which does not count as income and therefore is tax-free — to purchase coverage in the

Can I Live in a Different State than my Parents and Still be Covered on Their Health Insurance?

Yes, you can live in a different state and still be covered on your parent’s health plan up until age 26. However, keep in mind most health insurance plans distinguish between in-network and out-of-network care. If you live in another state, you may not be able to easily access in-network providers for your medical care. Out-of-network care is typically much more expensive than in-network care, often with its own separate

I Missed 2013 Open Enrollment for my Employer-Sponsored Plan. Will I Pay a Penalty for Waiting Until the Plan’s 2014 Open Enrollment?

The short answer is NO. The Internal Revenue will grant an exemption for the penalty tax as long as you enroll in coverage during your employer’s 2014 open enrollment period. Since health insurance became mandatory on January 1, 2014, the penalty exemption is available for people whose employer-sponsored plan has an open enrollment window that does not align with a calendar year. The issue really came about because, for this

- « Previous Page

- 1

- …

- 10

- 11

- 12

- 13

- 14

- …

- 26

- Next Page »